Where Can Indonesia's Trade Agreements Be Utilized?

Amid the current wave of international trade uncertainties -- triggered by geopolitical fragmentation, new protectionist policies, and commodity price volatility -- the utilization of bilateral and regional trade agreements is becoming increasingly strategic, even serving as a "safety net." This article examines the trade agreements Indonesia has participated in and negotiated from three dimensions: (1) the urgency of utilizing existing agreements, (2) the importance of negotiating new agreements, and (3) their synergy with national strategies.

Utilization of Agreements

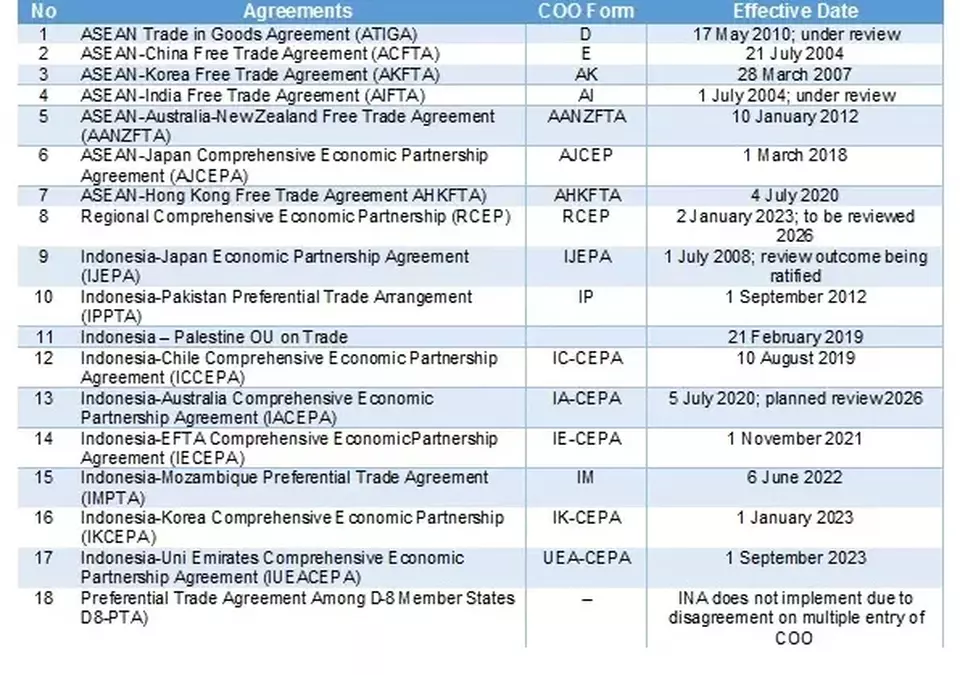

Indonesia currently has a network of FTAs (Free Trade Agreements), CEPAs (Comprehensive Economic Partnership Agreements), and PTAs (Preferential Trade Arrangements) with various partners, both bilaterally and regionally. In 2023, about 71.2 percent of Indonesia’s non-oil and gas exports were directed to fellow FTA/CEPA member countries. This is an increase from 69.2 percent in 2022. However, it should be noted that not all exports to FTA/CEPA partners utilize the preferential facilities offered by each agreement.

To utilize tariff preferences under these agreements, exporters must possess a document called a Certificate of Origin (COO). Currently, the application can be done through the Ministry of Trade’s e-COO system. Exporters need to submit an application and complete supporting documents, such as Export Notification of Goods (PEB), Invoice, Bill of Lading (B/L), and others. Once approved, the COO can be printed and signed by a company representative authorized to sign the COO for the products produced by the company they represent.

Unfortunately, the utilization rate of most agreements is not yet optimal, where the total value of Indonesia’s exports to FTA/CEPA/PTA countries is much higher than the export value taking advantage of preferential tariffs under the applicable FTA/CEPA/PTA umbrellas. There are several possible reasons why these agreements are underutilized. Among them are the lack of understanding by business actors about the procedures and benefits of tariff preferences; perceptions of high costs and complicated administration processes, especially for MSMEs; and insufficient understanding of compliance requirements such as technical standards, certifications, and other necessary criteria.

At the bilateral level, the low utilization of these trade agreements is quite noticeable. Data gathered by the Ministry of Trade from 2007 to 2024 shows varied but consistently low utilization performance of FTAs/CEPAs. For example, only 1.4 percent of Indonesia’s exports to Australia utilized IACEPA; 11 percent to EFTA countries used IECEPA facilities; 26.3 percent to Japan; 43.1 percent to the United Arab Emirates; 7.8 percent to South Korea; 73 percent to Pakistan (mostly CPO); and 0.1 percent to Mozambique.

Although the above utilization data is debatable as it overlaps with utilization data of regional agreements, serious efforts to optimize the agreements remain important amid global uncertainties. Markets already "guaranteed" preferential access through these agreements offer safer distribution channels compared to exporting outside FTA/CEPA frameworks, where the Most Favored Nation (MFN) tariffs apply. For example, when the US imposes high MFN or reciprocal tariffs on Chinese products, Indonesian exporters can leverage the ASEAN-China FTA or RCEP as Indonesia’s backward linkage to restructure supply chains to the US market while paying close attention to transshipment regulations.

The most tangible benefit of FTA/CEPA agreements is more open market access. For example, for HS 5513 to HS 5515 (woven fabric from synthetic staple fibers), the MFN import tariff applied by Australia is 5 percent. However, under the Indonesia-Australia CEPA bilateral agreement, this tariff becomes 0 percent.

Another example is the PTA between Indonesia and Pakistan. Since the agreement’s implementation in 2012, Indonesian CPO products have gradually displaced Malaysian CPO dominance in the Pakistani market. Before the PTA took effect, Malaysia’s market share of CPO in Pakistan was 62 percent, while Indonesia’s was 38 percent. However, Malaysia’s position has gradually shifted so that by 2016, Indonesia’s market share reached 82 percent, compared to Malaysia’s 18 percent. This market share advantage still holds today with slight variations each year.

New Agreements

Negotiating new agreements also becomes increasingly important in efforts to diversify markets amid globalization and fragmentation, like today. Dependence on a few key markets (such as China, the US, and Japan) tends to make exports more vulnerable in the case of economic or political shocks related to those countries. Currently, Indonesia has completed trade agreement negotiations with the European Union, Peru, the Eurasian Economic Union (Russia, Kazakhstan, Belarus, Armenia, and Kyrgyzstan), and is entering the legal scrubbing process before submission to each country’s parliament for ratification. Specifically with the European Union, there is already discourse to negotiate a region-to-region FTA between ASEAN and the EU in 2027; it seems the EU is waiting for its bilateral agreement with Indonesia to be effective first.

Meanwhile, Indonesia is also negotiating bilateral trade agreements with Canada and leading negotiations between ASEAN and Canada. Several other bilateral negotiations were launched some years ago but have not progressed seriously since the disruption of global supply chains due to Covid-19 and the US-China trade war, which made the FTA concept less popular. These have included Bangladesh, Sri Lanka, Tunisia, Turkey, exploration of negotiations with the GCC (Gulf Cooperation Council: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE), and MERCOSUR (Mercado Común del Sur: Argentina, Brazil, Paraguay, Uruguay, Venezuela, and Bolivia).

Another economically growing region is Africa. Indonesia needs to determine the approach: whether to negotiate bilaterally with several specific African countries or to negotiate with the African Continental Free Trade Area (AfCFTA), which covers 55 African Union member countries and whose agreement has been effective since January 1, 2021. While RCEP is the world’s largest FTA by market size (population) and total GDP, AfCFTA is the largest by the number of member countries.

Meeting commitments in existing agreements and negotiating new ones will bring benefits to Indonesia amid increasingly intense economic competition between nations. With trade agreements that provide certainty and offer tariff preferences, non-tariff measures, and trade and investment facilitation, Indonesia can secure market access to high-growth regions such as Latin America and Africa and increase Indonesia’s bargaining power in global supply chains, especially for value-added products.

Synergy with National Strategy

Negotiating and implementing trade agreements with other countries or groups must be linked to the national medium and long-term economic development strategy. Why? Because their impact on the resilience and competitiveness of the national economy is significant. While regional trade agreements are often referred to as "WTO plus" or deeper than WTO commitments, bilateral agreements are often described as "WTO plus-plus," meaning their commitments go even beyond regional agreements. Therefore, negotiating a trade agreement with other countries or groups must align with Indonesia’s efforts to adopt international best practices enshrined in the WTO, both in managing the national economy and engaging in rules-based international trade.

Opportunities opened through bilateral and regional trade agreements require Indonesia’s readiness to utilize them so they do not end up as mere piles of documents benefiting only the more aggressive partner. In the negotiation and utilization process, these agreements must align with national industrial development priorities, such as mineral downstreaming, the EV industry, and the digital economy. They must also consider the competitiveness of certain industries or sectors because market access means opening competition in the domestic market as well. Equally important is integrating national MSMEs into export supply chains. The government cannot leave MSMEs to compete freely in their own markets, relying only on large companies to benefit from these agreements.

In short, trade agreements like PTAs, FTAs, or CEPAs are strategic instruments to guarantee market access amid global disruption, reduce dependence on a handful of export markets, and strengthen Indonesia’s position in global supply chains. However, the key lies in two words: maximal utilization. Without it, the trade agreements Indonesia participates in will only become archives, not economic drivers.

---

Iman Pambagyo is the Trade Ministry’s Director General of International Trade Negotiations (2012-2014, 2016-2020) and Indonesia’s Ambassador to the WTO (2014-2015).

The views expressed in this article are those of the author.

Tags: Keywords:Related Articles

Indonesia Targets EU Trade Deal Ratification in 2026, Implementation by Early 2027

Indonesia aims to ratify its trade agreement with the European Union this year, paving the way for implementation in 2027.

When Import Permits Stall, Industry Suffers

When import permits are delayed without clarity, the risks extend beyond the companies directly involved.The Latest

Dear Mr. President, Don’t Skip ASEAN Summits

Despite calls for Prabowo to stay home, the Indonesian leader still needs to attend ASEAN summits.

PLN Rushes Coal Supplies After Power Outages Hit Java

PLN is rushing to secure coal supplies after shortages triggered rolling blackouts across Java, disrupting businesses and daily life.

Japan-Backed ADB Invests in Indonesia’s Human Capital

As many as 399 Indonesian awardees have joined the ADB-Japan Scholarship Program from 1988 to 2024.

Indonesian Stocks Rise Despite Foreign Outflows as MSCI Review Looms

Indonesia's JCI rose 2.8% as easing geopolitical tensions offset foreign outflows, MSCI concerns and rupiah pressures.